580. 670. 740. 800. These little three-digit numbers, known as credit scores, can have an enormous impact on your life.

When you apply for a credit card or loan, your credit score is a major factor in determining whether or not your application will be approved by a credit card company or bank. The higher the credit score you have, the more likely you are to be approved for homeowner and vehicle loans and to receive favorable interest rates. Your credit score even impacts the premiums of your vehicle and homeowners’ insurance.

Credit scores are also important when it comes to renting an apartment. Like lenders, landlords use credit scores to gauge whether an individual will make timely rent payments. That’s why a credit score check is almost always a part of the rental application process.

But what exactly is a credit score and how does one build a strong credit history? Read on to learn how your credit score is determined, why your credit score matters when apartment hunting, and how you can build better credit.

What is a credit score?

The three major credit reporting agencies are Experian, Transunion, and Equifax. They tabulate reports of payments made to credit card companies, lenders, and others. It’s all part of a process that yields what is known as a credit score.

A credit score is simply a numerical representation of an individual’s creditworthiness. It is a number ranging from a low of 300 to a high of 850. The higher the score, the better. There are five key items that go into a credit score. The impact of each varies slightly depending on the credit scoring model. Each item is weighted differently. These are common percentages:

- Payment history – 35%

- Amounts owed – 30%

- Length of credit history – 15%

- Credit mix – 10%

- New credit – 10%

Payment history includes payments made on credit cards, student loans, and installment loans. The number of accounts, hard inquiries and closed accounts are other factors. So is the age of your credit history. Accounts in collections, foreclosures, repossessions, and bankruptcies lower a credit score. Timely payments and low debt loads, on the other hand, tend to yield higher scores.

Credit scoring models

In 1989, the Fair Isaac Corporation developed a credit scoring model that became known by the acronym “FICO.” Over the years, there have been updates to the FICO model. For example, FICO 9, introduced in 2014, gives less weight to unpaid medical bills.

Although the FICO score is the most well known, there are other models used to calculate your credit score. VantageScore is a collaborative effort of Equifax, Experian, and TransUnion. VantageScore 3.0 includes up to 24 months of credit activity. It is even possible to include utility and rent payments in the calculations.

Credit scoring systems address different credit needs. FICO alone offers dozens of variations. For example, car dealers might use scores giving extra weight to timely car payments.

Factors not considered in credit scoring

There are also variables that don’t factor into a credit score:

- Age, salary, job title

- Gender, race, religious preference

- Interest rates you’re paying (on credit cards and installment loans, for example)

- Anything not proven to be predictive of future credit performance

- Soft inquiries

A soft inquiry, such as checking your own credit report, does not impact your credit score. A soft inquiry also occurs when you authorize an employer to check your report or when credit card companies check your credit report as they consider pre-approved offers.

Credit scores and the luxury apartment application process

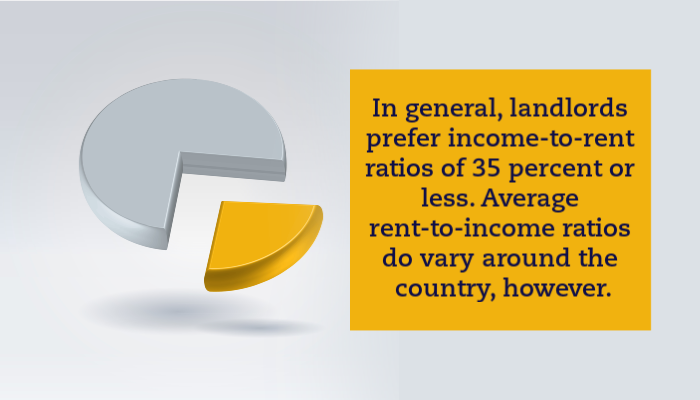

Landlords look at your credit score to evaluate your ability to pay the rent. Income and employment information are other factors. Income verification determines that the rent will not consume too much of what you earn.

In general, landlords prefer income-to-rent ratios of 35 percent or less. Average rent-to-income ratios do vary around the country, however. For example, it’s a relatively modest 28 percent in Chicago and a very high 45 percent in Los Angeles. Property owners often adopt standards prevalent in their area.

Landlords may disregard isolated credit blemishes resulting from certain one-time events. A late payment related to a medical payment several years ago is one example. It’s also important to note that every industry sees your credit through a particular lens. Late car payments are a red flag for landlords and could affect your application.

Credit issues and options

The higher the monthly rent, the greater the risk for the lessor and the greater the responsibility for the lessee. Landlords mitigate risk by using available metrics known to be predictive of success. Based on their experience, owners of luxury apartment properties fine-tune their credit standards over time. Their goal is to maintain a high occupancy rate while renting to those with the ability to make on-time payments.

Reporting timely rent payments

Traditionally, rent payments have not been reported to the credit bureaus. However, some landlords are now willing to do so upon request. For example, Yardi’s property management clients have the option of reporting rent payments to Experian RentBureau. This option can be very helpful to tenants who want to build their credit history with timely payments.

Key Takeaways

With a strong credit score, you can gain better interest rates on credit cards and loans, secure more affordable car insurance premiums, and improve your chances of approval on credit card and loan applications.

An impressive credit history can also make all the difference in helping you get approved for your dream apartment. If you’re searching for your next apartment, visit draperandkramer.com to learn more about Draper and Kramer’s portfolio of luxury apartments.